You are using an outdated browser. Please

upgrade your browser to improve your experience.

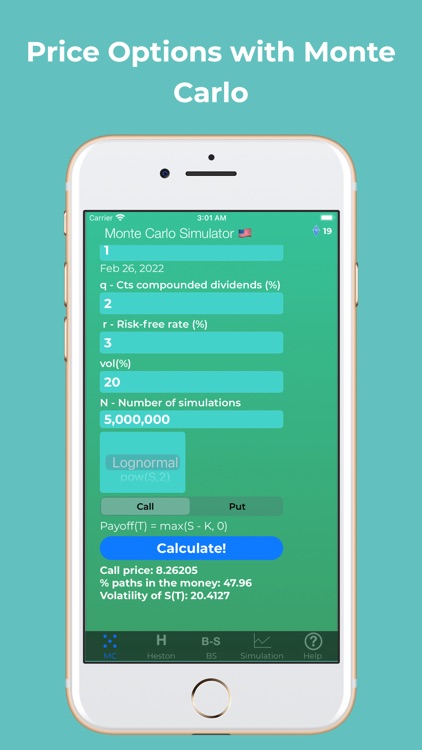

The Options Pricing Monte Carlo app prices power options: max(S^i -K,0) or max(K-S^i,0)

Options Pricing Monte Carlo

by Tenacious App Production, LLC

What is it about?

The Options Pricing Monte Carlo app prices power options: max(S^i -K,0) or max(K-S^i,0). It also shows the % of paths with positive payoffs. The normal inverse is calculated with Beasley-Springer-Moro method.

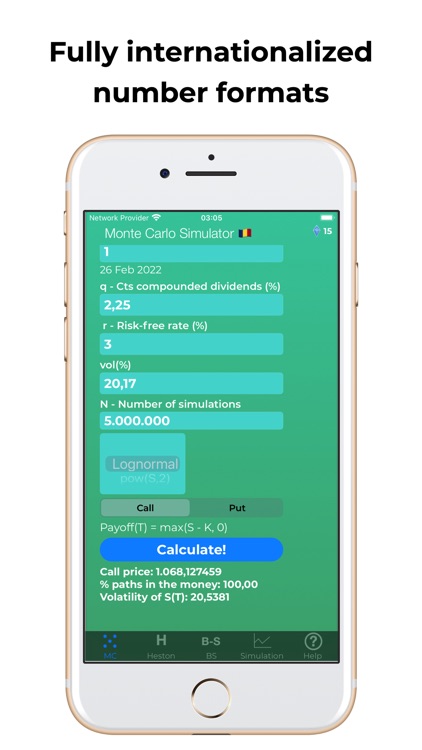

App Screenshots

App Store Description

The Options Pricing Monte Carlo app prices power options: max(S^i -K,0) or max(K-S^i,0). It also shows the % of paths with positive payoffs. The normal inverse is calculated with Beasley-Springer-Moro method.

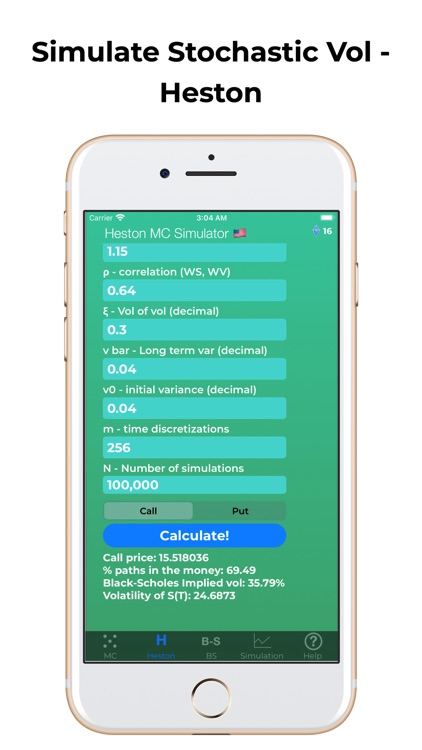

The Heston tab is used to price options under stochastic volatility using Monte Carlo.

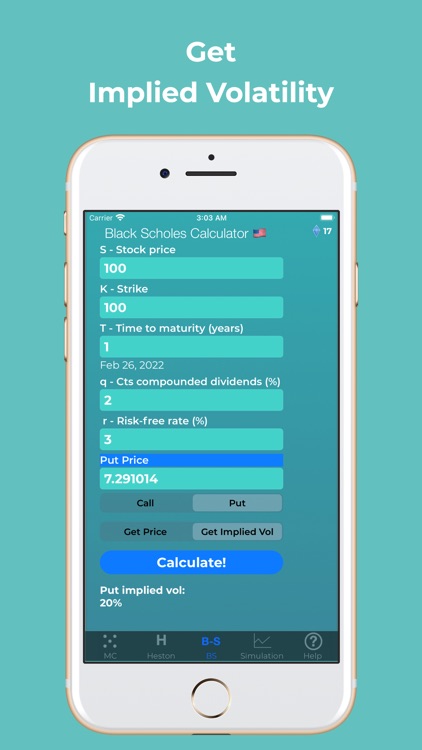

It also prices European options using Black-Scholes and can also calculate Implied Vol. Normal is calculated by direct integration using Simpson method with a low tolerance.

So 4 calculators in one:

- Monte Carlo simulator for regular European and Power options.

- Monte Carlo simulator for European options with stochastic vol (Heston model).

- Black Scholes calculator for price and greeks and implied vol.

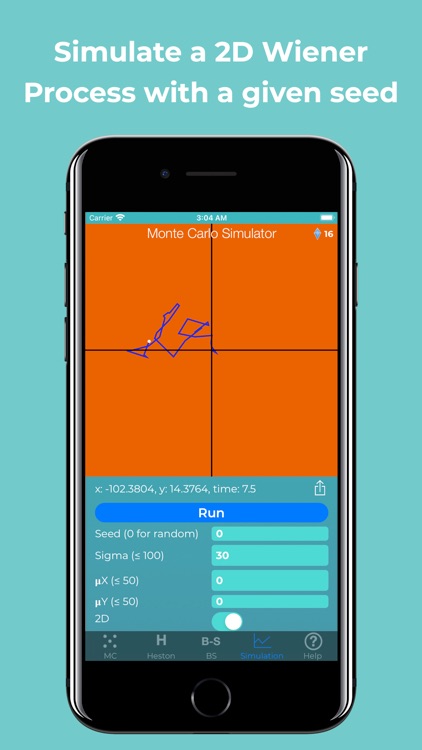

- Simulation tab lets you visualize Brownian Motion with drift. (2D or vs time).

Disclaimer:

AppAdvice does not own this application and only provides images and links contained in the iTunes Search API, to help our users find the best apps to download. If you are the developer of this app and would like your information removed, please send a request to takedown@appadvice.com and your information will be removed.

AppAdvice does not own this application and only provides images and links contained in the iTunes Search API, to help our users find the best apps to download. If you are the developer of this app and would like your information removed, please send a request to takedown@appadvice.com and your information will be removed.