You are using an outdated browser. Please

upgrade your browser to improve your experience.

"In probability theory and intertemporal portfolio choice, the Kelly criterion (or Kelly strategy or Kelly bet), also known as the scientific gambling method, is a formula for bet sizing that leads almost surely to higher wealth compared to any other strategy in the long run (i

Kelly Criterion Calculator

by Hergott Technologies, Inc

What is it about?

"In probability theory and intertemporal portfolio choice, the Kelly criterion (or Kelly strategy or Kelly bet), also known as the scientific gambling method, is a formula for bet sizing that leads almost surely to higher wealth compared to any other strategy in the long run (i.e. approaching the limit as the number of bets goes to infinity). The Kelly bet size is found by maximizing the expected value of the logarithm of wealth, which is equivalent to maximizing the expected geometric growth rate. The Kelly Criterion is to bet a predetermined fraction of assets, and it can seem counterintuitive. It was described by J. L. Kelly Jr, a researcher at Bell Labs, in 1956.

App Store Description

"In probability theory and intertemporal portfolio choice, the Kelly criterion (or Kelly strategy or Kelly bet), also known as the scientific gambling method, is a formula for bet sizing that leads almost surely to higher wealth compared to any other strategy in the long run (i.e. approaching the limit as the number of bets goes to infinity). The Kelly bet size is found by maximizing the expected value of the logarithm of wealth, which is equivalent to maximizing the expected geometric growth rate. The Kelly Criterion is to bet a predetermined fraction of assets, and it can seem counterintuitive. It was described by J. L. Kelly Jr, a researcher at Bell Labs, in 1956.

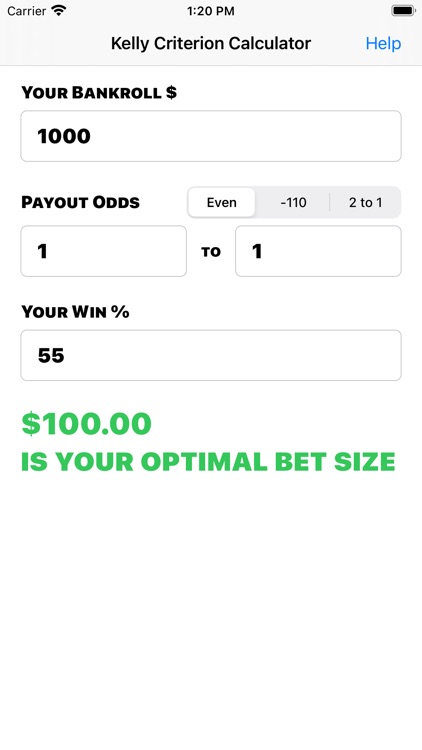

For an even money bet, the Kelly criterion computes the wager size percentage by multiplying the percent chance to win by two, then subtracting one. So, for a bet with a 70% chance to win the optimal wager size is 40% of available funds.

The practical use of the formula has been demonstrated for gambling and the same idea was used to explain diversification in investment management. In the 2000s, Kelly-style analysis became a part of mainstream investment theory and the claim has been made that well-known successful investors including Warren Buffett and Bill Gross use Kelly methods. William Poundstone wrote an extensive popular account of the history of Kelly betting."

- Wikipedia (https://en.wikipedia.org/wiki/Kelly_criterion)

Disclaimer:

AppAdvice does not own this application and only provides images and links contained in the iTunes Search API, to help our users find the best apps to download. If you are the developer of this app and would like your information removed, please send a request to takedown@appadvice.com and your information will be removed.

AppAdvice does not own this application and only provides images and links contained in the iTunes Search API, to help our users find the best apps to download. If you are the developer of this app and would like your information removed, please send a request to takedown@appadvice.com and your information will be removed.