You are using an outdated browser. Please

upgrade your browser to improve your experience.

The OPM App provides option pricing across numerous models for the following option types: Vanilla, Binary, Barrier, Lookback and Asian

OPM

by Rex Burdett

What is it about?

The OPM App provides option pricing across numerous models for the following option types: Vanilla, Binary, Barrier, Lookback and Asian.

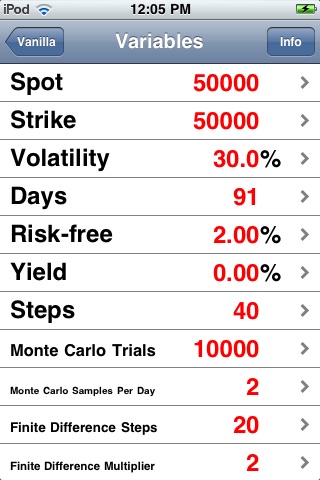

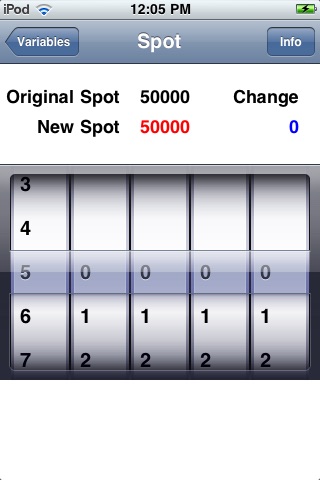

App Screenshots

App Store Description

The OPM App provides option pricing across numerous models for the following option types: Vanilla, Binary, Barrier, Lookback and Asian.

Viewing pricing variance across many different models provides a useful reality check.

Please be aware that the exotics may take a minute or two to calculate as will the vanilla options if the steps parameter is set high enough. Each price displayed represents a distinct model so it does take a little time to work through all the calculations.

Dependent upon applicability to the option type, the following pricing models are used:

- Black-Scholes (vanilla) and Black-Scholes type closed-form solutions (others)

- Monte Carlo simulation (trials and samples per day are user-input variables)

- various flavors of binomial and trinomial trees (time steps is a user-input variable)

- finite difference methods (implicit, explicit, and hopscotch - with and without change of variables - time steps and underlying multiplier steps are user-inputs)

- control variate

Contract user-input variables are (of course):

1) underlying (spot/future)

2) strike

3) volatility

4) days to expiration

5) risk-free rate

6) underlying yield.

For barrier options, barrier up and barrier down are user-input. Additionally, due to the lack of asian trees recombining, asian time steps are a separate input.

Disclaimer:

AppAdvice does not own this application and only provides images and links contained in the iTunes Search API, to help our users find the best apps to download. If you are the developer of this app and would like your information removed, please send a request to takedown@appadvice.com and your information will be removed.

AppAdvice does not own this application and only provides images and links contained in the iTunes Search API, to help our users find the best apps to download. If you are the developer of this app and would like your information removed, please send a request to takedown@appadvice.com and your information will be removed.